Money

-

Why Should I Care?

The amount of money in circulation is a really important issue in economics. It's going to affect your ability to get a loan to buy a house, or a car, and the price of everything else on the market.

-

This Lecture Has 7 Parts

- Definition and Role of Money

- Functions of Money

- Barter is Less Efficient

- What is Fiat Money

- What is Bitcoin

- What is Not Money

- Money Supply and Monetary Aggregates

-

What is Money?

Money is a good, a tangible product, made by the central banks of different countries. Money is generally accepted by the population, and used as final payment for resources, and final products. It serves a crucial role: helping people trade. Keep in mind that money is not a final good, you can't consume it. Money serves to allow transactions today, or to be saved, to allow future transactions.

-

Definition and Role of Money

Money is a good produced in the form of coins or paper notes. In Canada it is produced by the Bank of Canada as a service to the public. Money in bank accounts is also considered money; some call it “scriptural” money.

There are no laws forcing people to use Canadian dollars (CAD). However, there is a law prohibiting lenders to refuse money as payment for a debt. It is also illegal to print your own CAD bills. However, it is legal to produce your own money system. The value of our money relies solely on trust. There was a time when each dollar was backed by a gold coin, to generate trust, but that time is over. “Unbacked” money is called fiat money. Central banks can print as much fiat money as they see fit.

-

Functions of Money

Money has 3 functions:

Medium of exchange

I can buy things with it. It is accepted by other people on markets.

Unit of account

It’s divisible, I can count values and compare prices.

Store of value

I can keep it for later spending. It holds itits value over time, and doesn't depreciate.

Anything that does these three things could also be considered money, such as cigarettes in prison, or stickers at summer camp. In Canada, beaver pelts, playing cards, and gold coins were used as money in colonial times. The first money ever was obsidian arrowheads in the Armenian civilization, approximately 8,000 years BCE.

In Canada, the Canadian dollar is consideredrecognized as Legal Tender by the federal government. This means that this currency is recognized in law, so as to allow the settlement of debts before a court, and to settle tax liabilities with the State. The Canadian federal government reserves the right to refuse tax payments in other currencies than the Canadian dollar. It is not illegal to issue other currencies in Canada, but they cannot bear the mention 'legal tender' on the bills, so they would not be useableused to pay taxes or clear debts before a judge.

-

Barter is Less Efficient

Barter is great when it works. If you can find someone who wants what you have, and who has what you want, and both of you agree on the transaction (equal value), congratulations, you can make a trade. You are both better off. But this is hard to do on a regular basis. Sometimes people agree on the objects in the trade, but disagree on the value. Sometimes people agree on the value, but disagree on the objects.

That’s why it is usually more practical to sell to a third party, and then use money to buy a good. Money is therefore more efficient than barter to conduct transactions because you do not need double coincidence of wants and values.

This being said, a barter economy can be more efficient in some cases, when well organized (it needs coordination and planning), because it is sometimes simpler to produce than to earn money. This is true in simpler farming economies, for example. It can also have advantages for small businesses who can't efficiently monetize some of their production. Many entrepreneurs prefer to exchange services than to monetize the transactions. There are also examples of very large firms who resort to bartering in international trade situations, when the local political situation is uncertain.

-

What is Fiat Money

Commodity Money

Currency based on a mineral or metallic value, such as gold, silver, copper. The value of each coin is based on the value of its metal.

Standard Banking Money

Private banks print their own paper bills and keep minerals in reserve, usually gold. Also called Gold Standard. The value of each paper bill depends on the ratio of currency to gold.

Fiat Money

A central bank prints bills with no gold reserves. The use of the currency is supported by its legal tender. The value of the currency depends on both the stock of money and demand levels.

The origin of money is a fascinating topic. Many aspects of money are questioned to this day. Did people barter and then add coins to transactions? Did people use coins to measure debts and credits? Did people organize in command-style economies or in resource-sharing schemes? There are many ways to organize economies and to see them evolve over time.

The first cities are associated to the rise of money and mineral currencies. For example, the establishment of the first cities of the Armenian civilization were known to use money in the form of obsidian arrowheads, approximately 8,000 years BC. We know that metal coins appeared in Sumer, the central city-state of Mesopotamia 6,000 years BC. Metal coins became widely used in Asia, and Europe.

Originally, paper money wasappeared in 9th century in Tang dynasty China. Later European banks start to print money in places like Venice. This money has issued as a certificatecertificates to hold gold. Later, banks issued paper money, but it was still managed as gold certificate, the banks were holding gold to guarantee the value of their currency. In Canada, there were dozens of gold-standard banks (also called free banking or standard banking), until the Great Depression of 1929. Essentially, the gold-standard was in place until 1935, when the newly created Bank of Canada introduced its legal tender bank notes.

Money itself has become a central institution of modern society. The stability of the monetary system is thus very important for governments. It is also very convenient for governments to be able to print money to fund their projects, such as wars, or infrastructure. They also feel compelled to intervene during major economic recessions. Most governments thus have now undertaken to print the money of the land. However, most States do not wish to be beholden to a physically limited amount of money in circulation. Since they do not respect a gold-standard, or any commodity-asset limitations, and do not hold any physical asset to guarantee the value of the currency, we call this currency FIAT money.

Fiat is a latinLatin word that means “true by government decree”. Fiat currency (fiduciaire in French) is subject to much more inflation than gold-standard currency. This is because governments are free to print as much of it as they wish. The more they print, the less value the currency holds, and higher prices compensate this loss of value. Overprinting is the usual suspect when hyperinflation occurs.

-

What is Bitcoin

Bitcoin is a new currency that is not issued by a central bank. It is issued by an open code, and transactions are publicallypublicly published on “block chain” on the Internet. There are no metal coins, or paper notes. There are several of these crypto-currencies; this text refers only to the original Bitcoin currency.

The supply of Bitcoin is limited to 21 million “bitcoins”. However, each Bitcoin is divisible to the 100million decimal. So, if Bitcoins are worth 50,000 US dollars each, on an Internet market, an investor can easily buy 2 dollars worth on his or her phone. Bitcoins are exchanged electronically, usually with an “app” installed on a cellphone or a computer. In Canada, banks are not encouraging people to invest in Bitcoins. No one knows who created Bitcoins, which is usually a Buyer-Beware red-flag.

In Canada, Bitcoins are not regulated by the provincial securities authorities, such as the Ontario Securities Commission (OSC), or the Autorité des marchés financiers (AMF), in Quebec. The reason is that Bitcoin is not a vehicle for raising capital to fund a project. The Bitcoin currency is not considered a financial vehicle, such as a corporation or an investment firm. It is simply considered an asset, that can be thought of in the same way as rare art paintings, collector’s automobiles, or gold jewellery and coins. Any losses incurred on the Bitcoin market are not insured by governmental policies such as Canada’s Deposit Insurance. Banks usually do not offer Bitcoin accounts, although some trading platforms like Wealthsimple have come into this space, offering investment accounts in Canadian currency and crypto-assets.

Pros:

Each transaction incurs a very low transaction fee. Wiring money between banks across countries can be very expensive. It can cost up to 150 $ to send a few thousand Euros from a German bank to a Canadian bank. With bitcoins, the fee can be less than 15 cents. Also, there are no foreign exchange fees between the currencies.

The transactions are useable anywhere in the world that accepts Bitcoins. Japan has officially recognized the currency, and it stands in regular use in many other parts of the world. The validity of the “reserve of value” holds in the block chain which is a public document and available to be read by anyone in the world. Since the supply is fixed, the value of Bitcoins cannot depreciate if the number of users, and volume of trading increases. Bitcoins is therefore a potentially deflationary currency, which means it’s value increases over time. It becomes an investment in itself. This self-fulfilling prophecy has come to a grinding halt in 2022 as the trading of Bitcoin has slowed, and its price decreased substantially. What is true on the way up, is also true on the way down. Bitcoins have a fixed supply, but if no one is buying them, it's value drops.

Cons:

For now, the level of convenience is quite low. Specialized apps that allow one to trade Bitcoins are not as user-friendly as the use of a debit/Interac card, to make purchases, or the availability of cash machines (ATM). Usage depends on acceptance levels. As long as people don’t use it widely, it will not garner wide appeal.

Bitcoin is vulnerable to attacks from thieves. The bitcoin itself is not so vulnerable, it holds its value; that is why people want to steal it. But the apps that allow one to store Bitcoins in the “cloud”, which operate as your personal safe-house for crypto-assets, are not always using the best protection technology. This issue seems to have been resolved since the famous Mt. Gox heist, but caution is still necessary.

Since the supply is fixed, Bitcoins are a deflationary currency. That means people will hold it rather than use it daily, if they also have to use another currency which is less valuable. According to Gresham’s Law, when two currencies are in competition on a market, the fiat currency tends to be used more than the fixed-supply currency.

Being a recent development in the past decade, Bitcoins are an experiment and should be handled with great knowledge, healthy skepticism, critical thinking, and a balanced approach. One should never put all their eggs in the same basket.

Interview with Julien Brault - on Crypto Currencies

SummaryTable Table- Functions of Money Compared Across Assets

|

Asset Economic Function |

Canadian Dollar |

Gold coins |

Bitcoin |

|||

|

Cash |

Chequing Account |

Savings Account |

TFSA or RRSP |

|||

|

Medium of exchange |

+ |

++ |

- |

- |

- |

- |

|

Unit of account |

+ |

+ |

+ |

+ |

- |

++ |

|

Store of value |

-- |

-- |

+ |

++ |

+++ |

+++ |

|

|

|

|

|

|

|

|

|

Liquidity |

+++ |

++ |

- |

- |

- |

- |

|

Fungible / Untraceable |

+++ |

- |

- |

|

+++ |

+++ |

|

International Transfer |

- |

+ |

- |

- |

- |

+++ |

|

Pay taxes (Canada) |

+ |

+++ |

- |

- |

- |

- |

|

Legal Tender (clears debt) |

++ |

++ |

- |

- |

- |

- |

|

Will - Testament |

+ |

++ |

++ |

+ |

+ |

+ |

|

Safety / Robbery |

- |

+ |

+ |

+ |

- |

- |

|

Fiscal Advantage |

- |

- |

- |

++ |

- |

- |

|

|

|

|

|

|

|

|

|

Best use |

liquidity |

daily use |

saving |

investing |

storing |

transferring |

As you can see from the following graph, many countries have starkly different approaches to cryptocurrencies. There are only two countries who use Bitcoin as legal tender (as of June 2022). These are El Salvador and Central African Republic, two rather small countries. Many people believe Japan has enacted legal tender on Bitcoin, but this is not the case. Japan allows the use the cryptocurrency, but it does not enjoy the same legal provisions as the Yen.

Most of the Western world is allowing Bitcoin to be used in transactions and many countries impose capital gains tax on these transactions, such as Canada, the US, the UK, the European Union and Australia. Bitcoin is considered to be property, an asset, or a commodity depending on the country.

Table - Countries who ban, accept, and encourage Bitcoin (as of June 2022)

|

Ban |

Illegal | Legal | Legal Tender |

| Algeria | Bahrain | Australia | Central African Republic |

| Bangladesh | Burundi | Canada | El Salvador |

| China | Cameroon | Denmark | |

| Egypt | Gabon | Iceland | |

| Iraq | Georgia | European Union | |

| Morocco | Guyana | Japan | |

| Nepal | Kuwait | Mexico | |

| Qatar | Lesotho | United Kingdom | |

| Tunisia | Libya | USA | |

| Macao | |||

| Maldives | |||

| Vietnam | |||

| Zimbabwe | |||

Source: https://www.investopedia.com/articles/forex/041515/countries-where-bitcoin-legal-illegal.asp

The total amount of Bitcoin in circulation is 19 million coins, which are worth about 400 billion US dollars. This makes Bitcoin the 26th largest currency in the world, between the Polish Zloty and the Turkish Lira. The Canadian Dollar is worth 2.5 Trillion US dollars and is ranked 8th in world.

Table - World Currencies and Bitcoin

|

Rank |

Currency | Ticker | Circulation (in local currency) |

Exchange Rate |

Circulation $US |

| 1 | Chinese Yuan | CNY | 252 700 000 000 000 | 6.69 | 37 772 795 216 741 |

| 2 | United States Dollar | USD | 22 409 036 587 000 | 1.00 | 22 409 036 587 000 |

| 3 | Euro | EUR | 14 678 326 000 000 | 0.95 | 15 450 869 473 684 |

| 4 | Japanese Yen | JPY | 1 550 181 000 000 000 | 136.16 | 11 384 995 593 420 |

| 5 | Pound Sterling | GBP | 3 556 292 000 000 | 0.81 | 4 390 483 950 617 |

| 6 | South Korean Won | KRW | 4 977 732 000 000 000 | 1290.87 | 3 856 106 346 882 |

| 7 | Indian Rupee | INR | 208 194 000 000 000 | 78.10 | 2 665 736 235 595 |

| 8 | Canadian Dollar | CAD | 3 251 289 000 000 | 1.29 | 2 520 379 069 767 |

| 9 | Hong Kong Dollar | HKD | 16 387 404 000 000 | 7.85 | 2 087 567 388 535 |

| 10 | Australian Dollar | AUD | 2 702 000 000 000 | 1.43 | 1 889 510 489 510 |

| 26 | Bitcoin | BTC | 19 073 231 | 0.000047 | 405 813 425 532 |

Source: https://coinmarketcap.com/fiat-currencies/, Calculations by Author.

-

What is Not Money

-

Money Supply and Monetary Aggregates

When economists measure the stock of money in the economy, they don't include cheques and credit cards into the aggregate value.

First of all, a personal cheque is a promise to transfer money. It is an I-OWE-YOU note.

Second, the unused balance of credit cards are potential loans that are contracted at the time of purchase. A 1,000$ credit limit is not money, it is a potential loan. When the loan is contracted, money already accounted for will be transferred to the seller.

Interview with Julien Brault - on Credit Cards

It is possible to know exactly how much money is in circulation. This is a stock measurement. We also call it money supply or monetary mass. The simplest measure of money supply is called M1, which includes coins, notes, and savings accounts at chartered banks.

If you widen the definition, the stock of money is larger. There is no account of money supply for one province, such as Quebec. The larger the definition, the less liquid the types of accounts are included in the monetary aggregate. For example, if you wish to analyze M2++, you will need to consider that monies invested in Canada Savings Bonds, and mutual funds are not readily available to enact transactions. Those amounts are not liquid. Base money, or M1, which includes coins, paper notes, and debit card accounts (chequing), are quite liquid. You can use that money instantly to purchase something.

Table - Money Supply Aggregates in Canada

|

Aggregate |

Definition and scope |

Total M CAD |

|

Base Money |

Coins, paper notes, personal chequing accounts at chartered banks |

599,113 |

|

M1+ |

M1 + accounts at credit-unions and other non-bank deposit-taking financial institutions |

1,620,045 |

|

M2++ |

M1+ + mutual funds + Canada Savings Bonds |

4,434,934 |

Source: https://www.bankofcanada.ca/rates/indicators/key-variables/monetary-aggregates/

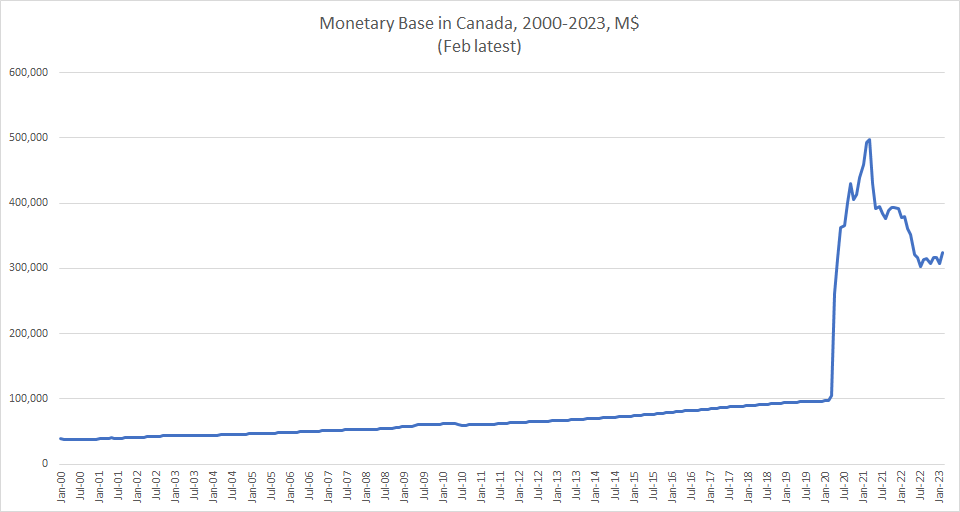

As you can see from the table above, there is quite a bit of money in circulation in Canada, but most of it is invested in long-term accounts like RRSPs and Pension funds. Given the electronic nature of currency nowadays, the most appropriate measure of liquid money supply would be M1+, which represented a stock of 1.6 trillion dollars in March 2022. As you can see on the graph below, money supply increases every year between 4 and 14 percent, to accommodate for the growth in the economy which is mostly driven by demographics. However, you can see that money supply has increased tremendously in the past few years to help finance government expenditure during the COVID-19 pandemic. The rate of increase in money supply has slowed, but the monetary aggregate is still growing. This has consequences for inflation, which is an important topic you need to learn about!

Graph - Money in Great Supply as of 2020

Source: Bank of Canada, 2022.

- Green Policy

Money has always been a source of environmental concern. But now it’s a form of pollution, especially in its virtual version. First of all, we’ve always mined gold and other minerals to produce money. We’ve cut trees to print money. And now, we burn fossil fuels to produce electricity to run server farms that house our virtual banking industry. When you use your debit card, servers need cooling to compute your transaction.

Bitcoins and cryptocurrency are making the situation worse. The chain-block ownership proofing process is a fascinating innovation in financial services. It allows to create new markets for currencies, but also for art, contracts, and personal wills. However, each time a transaction is conducted, the block-chain verification must follow the path down to the initial owner. So each time a new transaction is operated, the verification process takes a little bit more time, computer power, and server space. Cryptocurrency markets are incredibly large consumers of electricity and internet band-width. Since this is a new phenomenon, solutions are needed to reduce the environmental imprint of these new coins.

-

Climate Change Solution

If servers are running on fossil-fuel generated electricity, they are contributing to emissions of GHGs in the atmosphere. In order for the proliferation of Internet activities to continue sustainably, we must ensure that the electricity needed to run server farms comes from non-carbon sources, such as solar, wind, and hydro energy.

-

Democracy Booster

Bitcoins are creating a completely new currency market which may have consequences on many aspects of our societies.

Bitcoin itself is touted as a democratic ideal. It rests on perfect equality. Transactions are perfectly transparent – while keeping identities hidden. Transaction costs are ridiculously low, which makes it fair and open for all. Since the quantity of Bitcoins is fixed, it also protects investors from the possibility of dilution by a central bank.

However, Bitcoins also have a dark side. Safekeeping of bitcoins can be very expensive. Theft of bitcoins has seen people lose millions of dollars worth of savings. While many companies are offering to store cryptocurrency on behalf of persons, safety remains an issue.

Also, the anonymity of the transactions has attracted investors delving in criminal activity, making fungible currencies the money of choice for organized crime.

-

Wrap-Up

Money is a good generally accepted as final payment for resources and final products. It helps humans trade.

Any good that is a medium of exchange, a unit of account and a store of value could be used as money. Barter is inefficient because it needs double coincidence of wants. Cheques and credit cards are not money.

The Bank of Canada keeps track of money in circulation and calculates several monetary aggregates such as Base, M1+ and M2++.

Bitcoins and other cryptocurrencies are a new offering on money markets. Buyer beware.

-

Cheat Sheet

Barter:

Direct trade of goods without money.

Fiat money:

Paper money that is not backed by gold.

Legal tender:

Money recognized in law, usually to settle debts in court and to settle tax liabilities with the State.

Money:

An intermediate good that is generally accepted as final payment for resources, goods and services.

- References and Further Reading

AMF. (2022). Cryptoassets, What you need to know. Autorité des marchés financiers. Web. https://lautorite.qc.ca/en/general-public/investments/crypto

CNN. (2018). What is Bitcoin? Web. http://money.cnn.com/infographic/technology/what-is-bitcoin/

Davies, G. & Bank, J. H. (2002) A historyHistory of money:Money: fromFrom ancientAncient timesTimes to the presentPresent day.Day.

Feavearyear, A. E. (1963). The poundPound sterling;Sterling; a historyHistory of English moneyMoney. Oxford : Clarendon Press.

Ferguson, N. (2008). The ascentAscent of moneyMoney : a financialFinancial historyHistory of the worldWorld. New York : Penguin Press.

James, E., Wellman, S. J. & Aberra, W. (2010) Macroeconomics, 2nd ed. Pearson Canada. Chapter 13.

Smith, A. (1776). An Inquiry into the Nature and Causes of the Wealth of Nations. - Vol 1, Book 1, Ch. 4 - Of the Origin and Use of Money.

Weatherford, J. M. (1997). The historyHistory of moneyMoney : fromFrom sandstoneSandstone to cyberspaceCyberspace. New York : Crown Publishers.

Williams, J. (ed.) (1997). Money : a historyHistory. New York : St. Martin's Press.